From 6 April the Basic State Pension and Second State Pension (S2P) will end and be combined/ replaced by a new State Pension. Those who are paying reduced rate NI Contributions at the moment because they are in a work place pension scheme that is better than the Second State Pension will start to pay the standard NI contributions and start to earn a higher State Pension.

Who will it apply to?

This will apply to nearly all our members who are contributing to a workplace pension e.g. LGPS, NHSPS and private sector pension schemes.

How are National Insurance Contributions being calculated up to April 2016

If someone earns more than the Lower Earnings Limit currently £5824 a year (£112 a week) they will start to qualify for a State Pension. If they earn above what is called the ‘primary’ threshold currently £8060 a year (£155 a week) they start to pay NI contributions on earnings above that figure.

If they are in the Second State Pension they pay 12% on earnings up to the Upper Earnings Limit (£827 a week from April 2016) that is NOT in a work place pension that is contracted out of the Second State pension.

If on the other hand they are not in the Second State pension because they are paying into a work place pension instead that is contracted out of the Second State pension, they currently pay a reduced rate of 10.6% from the primary threshold up to what is called an ‘Upper Accrual Point’ of £770 a week and then pay 12% up to the Upper earnings Limit. On earnings above the Upper earnings limit the contribution goes down from 12% to 2 %

At the moment those who are contracted out also get a further small reduction on earnings between £5824 a year and £8060 a year.

How will National Insurance Contributions be calculated from April 2016

So after 6 April 2016 everyone will be paying 12% between £8060 a year and £43004 a year into the new State Pension. On earnings above Upper Earnings Limit of £43004 a year from April (£827 a week) they will continue to pay just 2%.

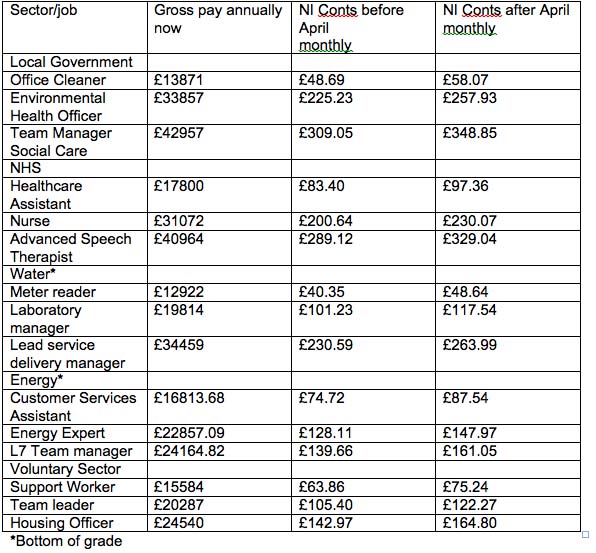

Set out below are some examples from the LGPS, NHSPS, Water, Energy and Voluntary Sector. They are purely illustrative of typical jobs and levels of pay in the sector. There may be small differences due to rounding in the NI calculations. The reduction in take home pay will be offset to certain degree by changes in tax thresholds from £10600 to £11,000 and if they receive a pay rise round April

Of course the person has to be a member of the relevant work place pension scheme. If they have opted out or haven’t joined; they already pay the higher rate.

Key Messages

For those who reach their State Pension Age after 5 April 2016 will have their State Pension calculated on the new basis. The full State Pension from 6 April 2016 will be £155.65 a week if a person has a minimum of 35 qualifying years and no contracted out service in a work place pension scheme like the LGPS,NHPS etc...

If you have a lot of contracted out service and you would have qualified for the pre April Basic State Pension your minimum new State Pension at 6 April 2016 will be the single person’s Basic State Pension of £119.30 a week from April not the £155.65 a week.

If you are still working after April and earning above the lower earnings limit you will earn extra pension up to the maximum of £155.65 a week (this will be increased in line with the better of average earnings, inflation (CPI) or 2.5%).

If your State Pension is less than £155.65 per week you can earn extra state pension up to your State Pension Age or until you reach the maximum pension that starts at £155.65, whichever occurs first. For every year you pay at the higher rate you would be earning based on the starting pension, £4.45 a week extra pension until you reach State Pension Age or you reach the maximum State Pension (that is 1/35 X £155.65 = £4.45 a week).

So for most of our members in workplace schemes they will be paying more NI but earning extra State Pension at a very reasonable price.

The new full State Pension is still below the poverty line so members should not leave their workplace pension scheme.

In the LGPS where the opt out rates are highest amongst low paid staff the message is if you feel you cannot afford the higher NI and stay in the LGPS consider electing to pay half your normal contributions to the LGPS to get a lower benefit until you can afford to pay at the full rate again.

Everyone should apply in writing or on line for an up to date state pension statement

https://www.gov.uk/government/publications/application-for-a-state-pension-statement

What are the other issues?

There is a big issue on who will pay the pension increase on the part of the workplace pension the member would have got if they had contributed to the Second State Pension instead of their workplace pension.

Until April this increase has mainly been paid as an addition to the state pension. From April depending on the rules of the scheme either the pension scheme will now have to pay or it simply won’t increase in line with inflation anymore for anyone who reaches State Pension Age after April 2016.

Public Sector schemes like the LGPS and NHSPS would pay the increase unless the government allows them to change the rules. Good news for members, but another burden on the schemes that could feed into further cuts and job losses.

There is a danger that a number of women and men who reach state pension age after April will be worse off as spouses pensions attached to the basic state pension are being withdrawn. They will not be able to increase their state pension using their spouse or civil partner’s (or late or former spouse or civil partner’s) NI contributions but if they are widowed they may still be able to inherit some additional State Pension under transitional rules.

The increase and equalisation in State Pension Age has meant that particularly women born in the first half of 1950’s are being faced with a larger than expected increase in their State Pension Age. The government is being pressured into looking again at the transitional period and possible compensation for women whose State Pension Age is set to rise by more than a year by April 2020. There is a petition with currently 148,000 signatories and ongoing debates in parliament.

https://petition.parliament.uk/petitions/110776

For those who reach their State Pension Age after 5 April 2016 will have their State Pension calculated on the new basis. The full State Pension from 6 April 2016 will be £155.65 a week if a person has a minimum of 35 qualifying years and no contracted out service in a work place pension scheme like the LGPS,NHPS etc...

If you have a lot of contracted out service and you would have qualified for the pre April Basic State Pension your minimum new State Pension at 6 April 2016 will be the single person’s Basic State Pension of £119.30 a week from April not the £155.65 a week.

If you are still working after April and earning above the lower earnings limit you will earn extra pension up to the maximum of £155.65 a week (this will be increased in line with the better of average earnings, inflation (CPI) or 2.5%).

If your State Pension is less than £155.65 per week you can earn extra state pension up to your State Pension Age or until you reach the maximum pension that starts at £155.65, whichever occurs first. For every year you pay at the higher rate you would be earning based on the starting pension, £4.45 a week extra pension until you reach State Pension Age or you reach the maximum State Pension (that is 1/35 X £155.65 = £4.45 a week).

So for most of our members in workplace schemes they will be paying more NI but earning extra State Pension at a very reasonable price.

The new full State Pension is still below the poverty line so members should not leave their workplace pension scheme.

In the LGPS where the opt out rates are highest amongst low paid staff the message is if you feel you cannot afford the higher NI and stay in the LGPS consider electing to pay half your normal contributions to the LGPS to get a lower benefit until you can afford to pay at the full rate again.

Everyone should apply in writing or on line for an up to date state pension statement

https://www.gov.uk/government/publications/application-for-a-state-pension-statement

What are the other issues?

There is a big issue on who will pay the pension increase on the part of the workplace pension the member would have got if they had contributed to the Second State Pension instead of their workplace pension.

Until April this increase has mainly been paid as an addition to the state pension. From April depending on the rules of the scheme either the pension scheme will now have to pay or it simply won’t increase in line with inflation anymore for anyone who reaches State Pension Age after April 2016.

Public Sector schemes like the LGPS and NHSPS would pay the increase unless the government allows them to change the rules. Good news for members, but another burden on the schemes that could feed into further cuts and job losses.

There is a danger that a number of women and men who reach state pension age after April will be worse off as spouses pensions attached to the basic state pension are being withdrawn. They will not be able to increase their state pension using their spouse or civil partner’s (or late or former spouse or civil partner’s) NI contributions but if they are widowed they may still be able to inherit some additional State Pension under transitional rules.

The increase and equalisation in State Pension Age has meant that particularly women born in the first half of 1950’s are being faced with a larger than expected increase in their State Pension Age. The government is being pressured into looking again at the transitional period and possible compensation for women whose State Pension Age is set to rise by more than a year by April 2020. There is a petition with currently 148,000 signatories and ongoing debates in parliament.

https://petition.parliament.uk/petitions/110776

RSS Feed

RSS Feed